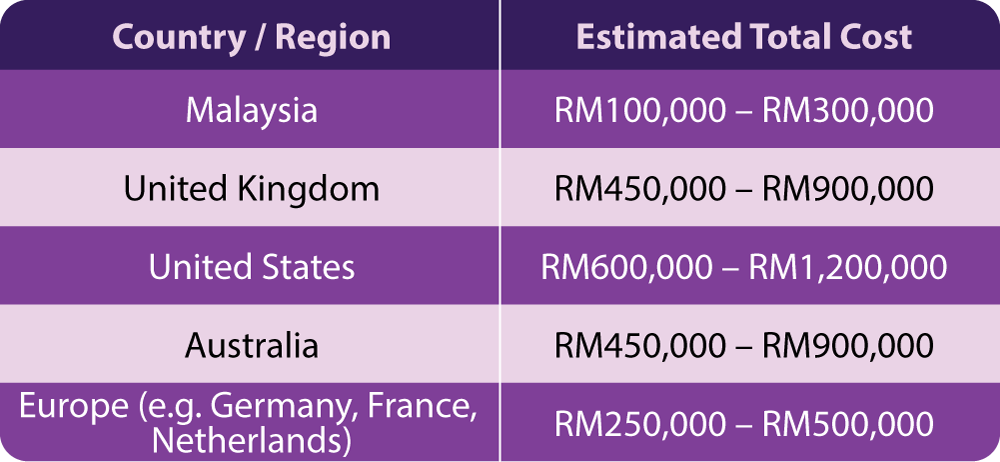

Estimated Total Cost of a Degree (3–4 Years)

For many Malaysian parents, the education fund needed is between RM500,000 and RM1 million.

• Watch out for hidden fees (bank charges, exchange rates)

• Make use of student discounts

• Optimise living costs by adopting local spending habits

Source:

Child age: 5

University start: 18

Time horizon: 13 years

Target education fund: RM700,000

Estimated monthly savings needed:

Key Insight:

The earlier you start, the lower your monthly commitment.

Estimated Total Cost of a Degree (3–4 Years)

For many Malaysian parents, the education fund needed is between RM500,000 and RM1 million.

• Watch out for hidden fees (bank charges, exchange rates)

• Make use of student discounts

• Optimise living costs by adopting local spending habits

Source:

Child age: 5

University start: 18

Time horizon: 13 years

Target education fund: RM700,000

Estimated monthly savings needed:

Key Insight:

The earlier you start, the lower your monthly commitment.